This is a summary of links featured on Quantocracy on Sunday, 04/24/2016. To see our most recent links, visit the Quant Mashup. Read on readers!

-

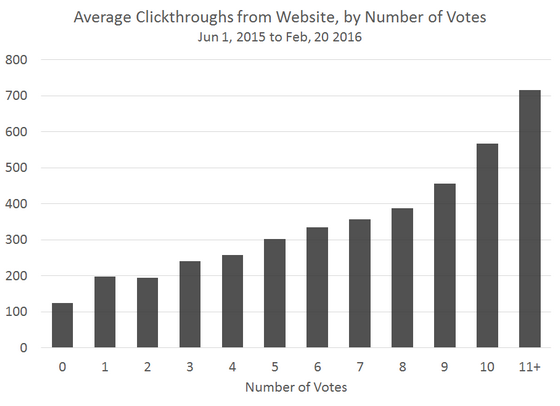

Best Links of the Last Two Weeks [Quantocracy]The best quant mashup links for the two weeks ending Saturday, 04/23 as voted by our readers: Lossless Compression Algorithms and Market Efficiency? [Turing Finance] You cant beat all the chimps [Following the Trend] My Year-Long Experience as the Fastest Form-4 Trader [Greg Harris] Are 3-year track records meaningful? [Flirting with Models] The Changing Generations of Financial Data [Quandl]

-

New Book Added: Intro to Statistical Learning with Applications in R [Amazon]An Introduction to Statistical Learning provides an accessible overview of the field of statistical learning, an essential toolset for making sense of the vast and complex data sets that have emerged in fields ranging from biology to finance to marketing to astrophysics in the past twenty years. This book presents some of the most important modeling and prediction techniques, along with relevant