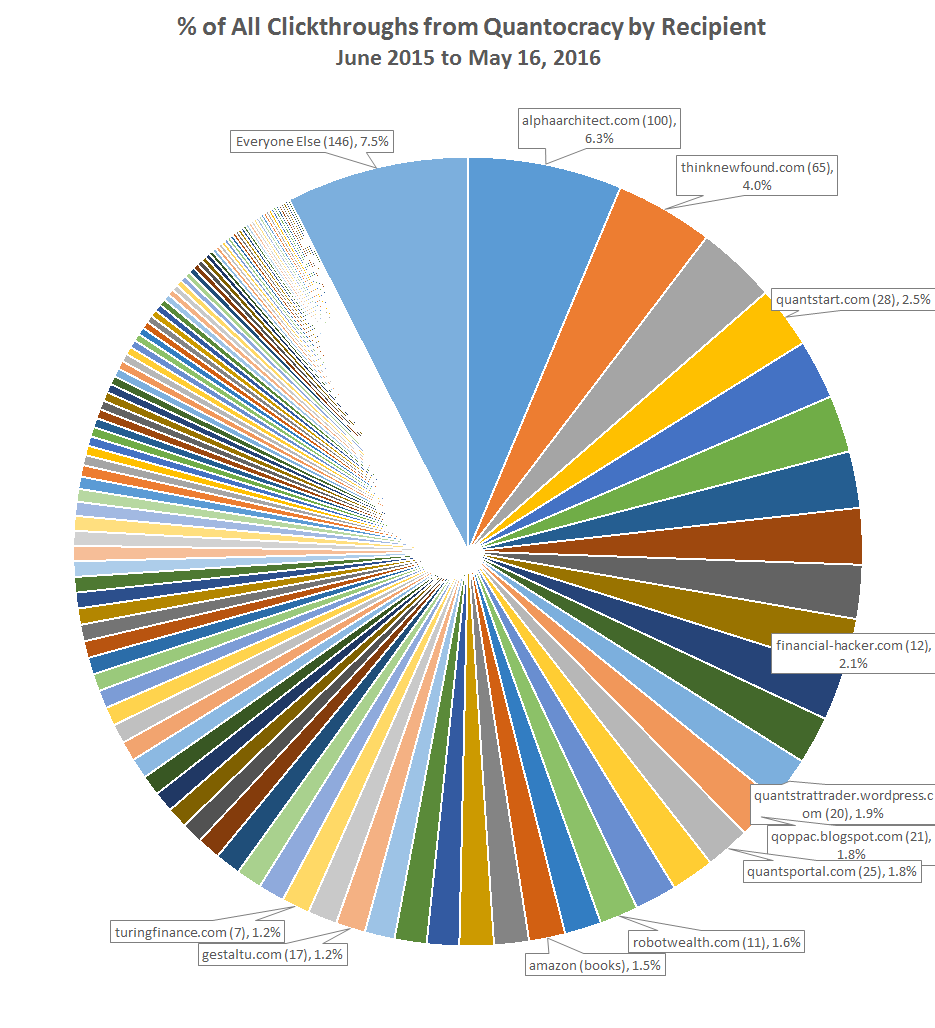

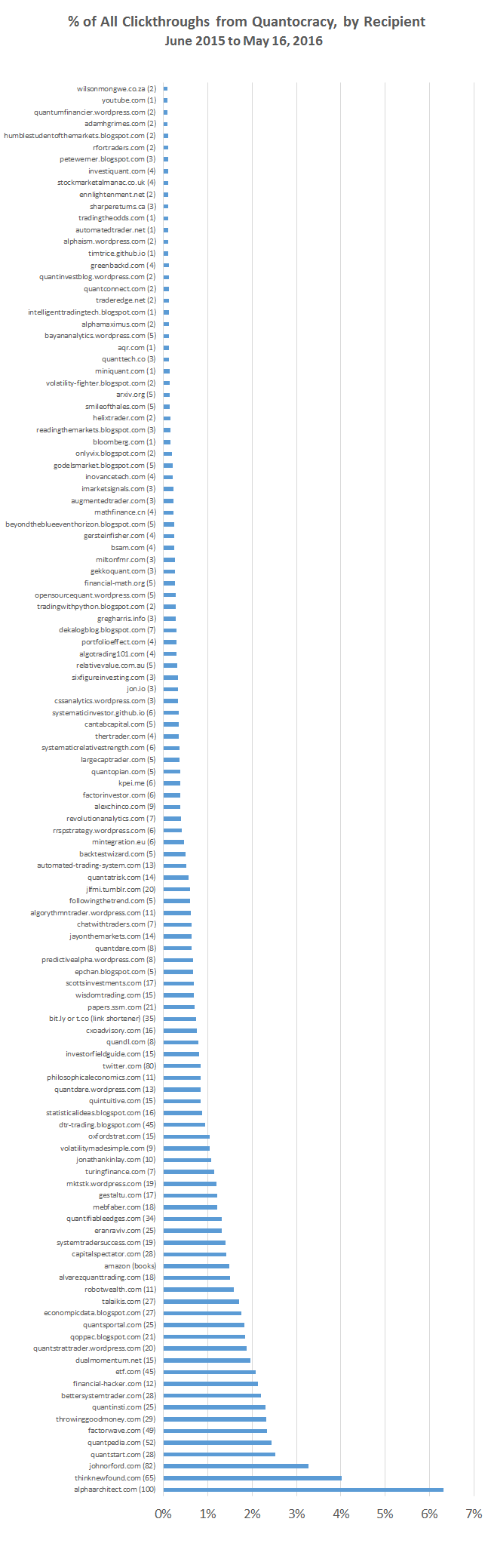

This is a summary of links featured on Quantocracy on Wednesday, 05/18/2016. To see our most recent links, visit the Quant Mashup. Read on readers!

-

Optimising weights with costs (pysystemtrade) [Investment Idiocy]In a previous post I showed you how to use my open source python backtesting package, pysystemtrade, to estimate forecast weights and instrument weights. At the time I hadn't included code to calculate costs. Now that has been remedied I thought I should also write some code to demonstrate the different ways you can optimise in the presence of costs. You can see what else has been included in

-

A Stunning New Finding: Return Seasonalities are Everywhere [Alpha Architect]Weve discussed return seasonalities in the past, especially as they pertain to our approach to momentum. Turns out seasonality effects arent confined to momentum they are literally everywhere and they are incredibly strong. This paper will blow your mind once you let the results settle in a bit. Source paper Slides Turns out stock returns are lumpy across the calendar. Stocks dont

-

Machine Beats Human: Machine Learning in Forex [Jon.IO]Machine learning and trading is a very interesting subject. It is also a subject where you can spend tons of time writing code and reading papers and then a kid can beat you while playing Mario Kart. In the nexts posts, we are going to talk about: Optimize entries and exits. This and only this could make a ton of difference in your bank roll. Calculate position size (in case you don't like

-

Which Institution Has The Best Asset Allocation Model? [Meb Faber]If youre like most investors, youre asking the wrong questions. I was chatting with a group of advisors this week down in La Jolla and a question arose. Ill paraphrase: Meb, thanks for the talk. We get a steady stream of salespeople and consultants in here hawking their various asset allocation models. Frankly, it can be overwhelming. Some will send us a 50-page report, all to explain

-

The State of Risk Management [Flirting with Models]How effective is your method of managing portfolio risk? We compare and contrast different approaches including fixed income, managed futures, low volatility equities, and tactical to explore the relative protection they can deliver versus the return drag they can create.

-

World s Simplest Trading System [UK Stock Market Almanac]Heres the system: At the end of every month, if the index is above its 10-month simple moving average: the portfolio is 100% in the market if the index is below its 10-month simple moving average: the portfolio is 100% in cash And thats it. So, if we take the FTSE 100 Index as an example, if at the end of a month the FTSE 100 is above its 10-month simple moving average then either, the