The best quant mashup links for the two weeks ending Saturday, 06/25 as voted by our readers:

- Recommended Reading [Robot Wealth]

- Binary Options: Scam or Opportunity? [Financial Hacker]

- Some harmless data-mining: Testing individual words in EDGAR filings [Greg Harris]

- Simple Machine Learning Model to Trade SPY [Alpha Plot]

- Want to Know the Secret to Inefficient Prices? Lazy Prices. [Alpha Architect]

- Strategy Evaluation with Dave Walton [Better System Trader]

There have also been some well received links from new blogger Tulip Quant. Unfortunately, Tulip’s site has been having technical difficulties as of late, so I didn’t include his links here, but if the site is up when you read this, I would recommend hopping over and having a look.

* * *

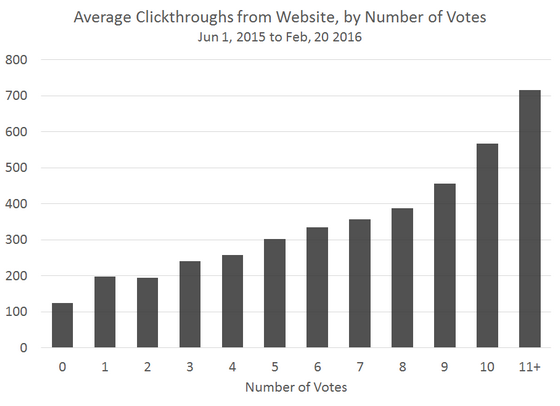

[click graph to enlarge]

The graph to the right shows the average number of clickthroughs a link receives from our website (excluding RSS, Twitter and Stocktwits), broken out by the number of votes cast by our readers.

A core goal of Quantocracy is to have a positive impact on our corner of the financial world by rewarding the best work, and encouraging the best minds to keep writing.

As the graph makes clear, the citizens of Quantocracy are doing just that (way to go guys). Links with 11 or more votes receive nearly 6-times as many clickthroughs as a link with no votes (wow).

If you haven’t done so already, we invite you to register to vote and be a part of the effort. Your votes matter to the quant community.

Read on Readers!

Mike @ Quantocracy