Two bits of site news:

First, after 4+ years of running this site mostly gratis, I’ve decided to dabble in adding advertisements, so expect to begin seeing the first baby steps with a handful of ads from Google. I’ve tried to keep the ads as unobtrusive as possible and my hope is that your reading experience will be essentially unchanged.

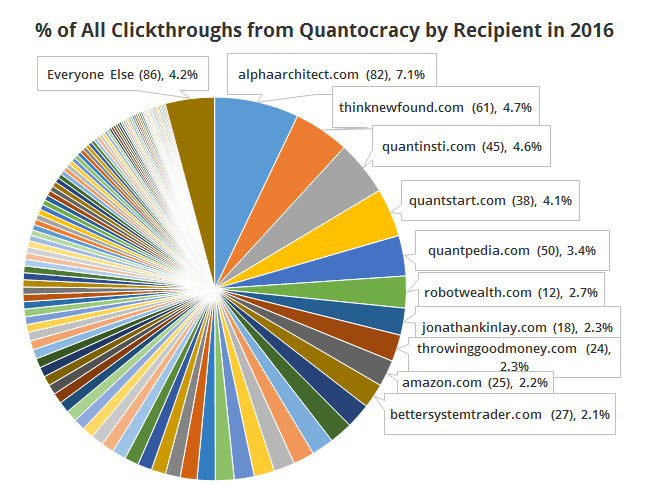

On to more fun news, here’s an updated view of where the all the clicks on the mashup went in 2016. The numbers include any site that received at least 500 clicks, but ignore our Twitter, Stocktwits and daily RSS/Email.

I’ve labeled the top 10 recipients. The number in parenthesis represents the number of links we carried from that site, and the % represents the portion of all clicks that that site received.

Alpha Architect remains the top dog at 7.1% of clickthroughs (how they maintain their amazingly consistent publishing schedule I’ll never know).

We’re casting a wide net though. The top 10 recipients together only received about 35% of total clickthroughs. A whopping 117 sites received at least 500 clickthroughs for the year. I’m happy with that. The goal of Quantocracy is to improve not just the quality of work in the quantitative blogosphere (read more), but the quantity as well.

At no point in history has so much good work on these subjects been shared so freely. To all of the denizens of Quantocracy: a big mahalo, gracias, 謝謝 and thank you for helping this community to grow.

And finally, the 5 most clicked links of the year:

- Machine learning for financial prediction: experimentation with Aronson’s work – part 1 [Robot Wealth]

- Machine learning for financial prediction: experimentation with Aronson’s work – part 2 [Robot Wealth]

- Recommended Reading [Robot Wealth]

- A simple breakout trading rule (pysystemtrade) [Investment Idiocy]

- Get Rich Slowly [Financial Hacker]

Read on Readers!

Mike @ Quantocracy